CRE CLO Comeback

October 14, 2025

Executive Summary

With more than $17 billion in issuance through mid-2025, new-vintage CRE CLOs are repricing risk but channeling bridge capital to transitional assets such as retail-to-storage conversions.

Commercial real estate (CRE) collateralized loan obligations (CLOs) have made an unmistakable comeback in 2025 — but this is not a return to the froth of 2021. Instead, the market is being carefully rebuilt: higher coupons, tighter underwriting, and a renewed focus on cash-flowing assets. For high net worth (HNW) investors looking to allocate to private-credit and structured-credit strategies, the comeback offers an intriguing mix of yield, selectivity and — importantly — new channels of capital into transitional properties such as retail-to-self-storage conversions.

Here’s the layman’s summary: Commercial real estate CLOs are basically bundles of short-term property loans that investors can buy into, and they’ve started making a comeback in 2025. This time, lenders are being more careful — focusing on properties that already make money instead of risky bets — which creates safer ways for investors to earn steady income.

Why the 2025 rebound matters

After a contraction in 2023, new-vintage CRE CLO issuance surged in the first half of 2025. Trepp reports more than $17 billion of new CRE CLO issuance through mid-2025 — a volume signal that investors are once again willing to finance CRE loans packaged into CLOs. But unlike prior cycles, the new issuance reflects a repricing of risk: higher debt yields, stronger Debt-Service Coverage Ratios (DSCRs) and more conservative sponsor assumptions.1

What makes this relevant for HNW investors:

- CLO structures provide floating-rate and fixed-rate tranches, enabling yield capture in a higher-rate environment.

- New-vintage CRE CLOs are underwriting more cash-flow support (higher DSCRs), reducing the chance that coupon resets or refinancings immediately stress the capital stack.

- Transitional asset exposure (e.g., self-storage conversions) gives investors access to value-add CRE themes that are operationally driven rather than purely speculative.

The data — the comeback in numbers

A few load-bearing facts worth leaning on:

- $17B+ in CRE CLO issuance through mid-2025, per Trepp — a rebound in volume and a signal of renewed market access. 2

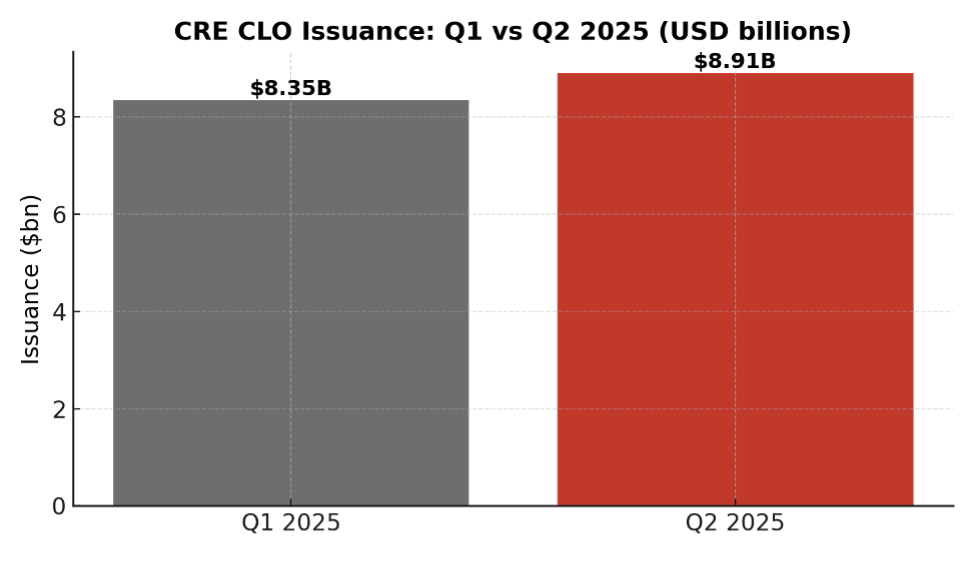

- Q1 and Q2 2025 issuance were strong: ~$8.35B (Q1) and ~$8.91B (Q2), reflecting a rapid readmittance of issuance activity into the market. (These quarter numbers add up closely to Trepp’s mid-year total.) 11

- Vintage underwriting is materially different: recent cohorts show weighted average DSCRs above 1.3x and debt yields well into double digits (e.g., debt yield ~15.65% vs coupon ~8.07% in a Q2 cohort example), indicating lenders are building meaningful cash-flow cushions.3

What’s changed in underwriting and structure?

This is not a simple “more issuance” story. The makeup of the new deals shows a deliberate repricing and restructuring of risk.

- DSCR and debt yield focus. Originators are prioritizing in-place cash flows (higher DSCRs) and anchoring pricing to debt yield rather than rosy projections. Recent cohorts show DSCRs in the 1.3x range versus sub-1.0x vintages from 2021–2023.4

- Sector tilting. Multifamily still dominates issuance (it accounts for the lion’s share of 2025 issuance), while exposure to office has fallen to near-zero as issuers sidestep transitional office risk. Lenders are, however, expanding “other” buckets that include self-storage, lodging and niche assets viewed as operationally resilient.5

- Coupon reality. Borrowers are paying materially higher coupons versus the low-rate era; lenders are seeking a wider spread between debt yield and coupon to create a buffer for credit stress. That means better protection for CLO tranche investors if originators maintain disciplined underwriting.6

Where the capital is flowing: transitional assets and adaptive reuse

One of the most visible narratives of 2024–2025 is how capital is finding transitional opportunities — notably retail-to-self-storage and other adaptive-reuse plays.

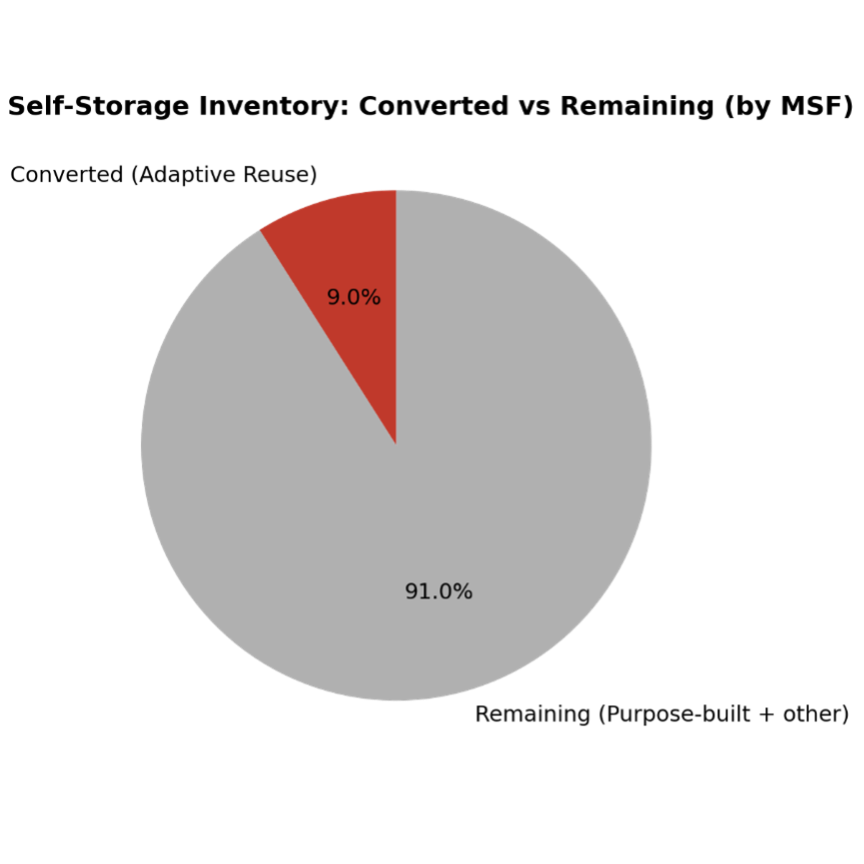

Adaptive reuse into self-storage now represents roughly 191 million square feet of converted space — about 9% of the U.S. self-storage inventory, according to CRE Daily/StorageCafe data. These conversions (former retail, industrial or big-box sites) are attractive for several reasons: faster speed-to-cash, lower land costs, and stable local demand for storage. 12

Converted facilities often deliver rent parity or slight savings vs purpose-built units and can open an operating cash-flow path more quickly than ground-up development — an appealing profile for loans packaged into new-vintage CRE CLOs. 13

Why CRE CLOs are attractive to HNW investors now

For an investor with HNW objectives — capital preservation plus attractive income — the new CRE CLO vintage offers features worth considering:

- Higher starting yields: CLO debt tranches and even equity tranches in conservative structures can offer compelling spreads vs public credit alternatives.

- Floating-rate protection: Many CRE CLO tranches are linked to short-term rates; in a rising or uncertain rate regime, floating rate exposure hedges duration risk.

- Diversification access: CRE CLO collateral pools include many loans across property types — multifamily, self-storage, industrial, lodging — which can smooth idiosyncratic asset shocks when properly underwritten.

- Sponsor alignment and diligence: Post-2023, underwriters and CLO managers are emphasizing stronger covenants and more transparent vintage reporting — beneficial for select investors who do the diligence. 7

Risks (The Honest Checklist)

No investment is without risk. CRE CLOs bring specific considerations:

- Refinancing and reset risk in older vintages. Legacy loans with weak DSCRs from the low-rate era can still stress CLO cash flows and create pressure points during reinvestment or reset periods. Investors should separate old vintages from new underwritten vintages in their analysis. 8

- Asset-specific operating risk. Conversions (retail→storage) generally look attractive, but success depends on location, zoning, construction execution, and operator expertise. Sponsor risk matters. 14

- Concentration & structural complexity. CLOs can be complex; tranche mechanics, subordination levels and manager decisions matter. HNW investors should demand transparency and stress-test waterfall scenarios.

Due diligence playbook for HNW investors

If you’re evaluating allocations to CRE CLO strategies or specific CLO tranches, here’s a concise checklist of topics you’ll want to explore:

- Manager & track record: depth of CRE underwriting and prior CLO performance.

- Vintage inspection: isolate 2024–2025 cohorts with DSCR and debt-yield metrics vs older vintages.

- Collateral composition: percent multifamily, industrial, self-storage, office exposure.

- Covenant quality: floors on DSCR, loan-to-value (LTV) protections and seasoning requirements.

- Liquidity and secondary market: tradeability of the tranche and manager reinvestment policies.

- Scenario modeling: run 200–300 bps stress tests on cap rates, vacancy and rent growth.

Trepp’s vintage metrics — showing improved DSCRs and debt-yield spreads for 2024–2025 cohorts — are exactly the sorts of data investors should request and model into downside scenarios.9

Expert voice — context from the market

Thomas Taylor of Trepp observed that the 2025 comeback “marks a clear shift in how lenders, borrowers, and investors are approaching credit, structure, and property risk.” He notes that this year’s cohorts reflect “improved performance” and a “sharp rebalancing toward actual income rather than anticipated upside.” That language captures the essence of the new vintage: income first, assumptions second. 10

Industry reporting adds nuance: market commentators note that while issuance has recovered, the tone is “cautious” — a reminder to separate volume from credit quality in any allocation decision. 15

How CRE CLOs can fit into a diversified HNW portfolio

- Income barbell: Use a portion of the private credit allocation to buy short-duration CRE CLO debt tranches (income + floating rate) alongside longer-term private equity CRE plays.

- Opportunistic exposure: Consider a small tactical allocation to CRE CLO equity for investors who understand mezzanine risk and want higher upside — but only after stress-testing waterfall scenarios.

- Sponsor co-investments: Where possible, pursue direct or co-investment opportunities alongside experienced managers to capture sponsor alignment and fee efficiencies.

Bottom line — cautious optimism.

The CRE CLO market’s return in 2025 is meaningful: capital is flowing, underwriting is resetting, and risk is being repriced. That creates opportunities — particularly for well-informed HNW investors — to capture income and participate in transitional CRE themes (like retail-to-storage conversions) that benefit from operational execution more than speculative valuation growth.

But the playbook is different from the last cycle. Success requires active due diligence, vintage discernment, and a focus on cash-flow metrics over future-value assumptions. For investors who demand yield and want exposure to CRE credit with structural protections, new-vintage CRE CLOs deserve attention — provided they’re approached with rigor and an eye for quality managers.

-------

Sources:

1 - 10 = CRE CLO Issuance in 2025: A Rebound in Volume; A Repricing of Risk (Thomas Taylor). Provides mid-2025 issuance figure, vintage DSCR and debt-yield detail. trepp.com

11 - 14 = Self-Storage Conversions Expand… and related briefing; details on 191 MSF converted and 9% of U.S. inventory. CRE Daily

15 = GlobeSt (analysis pieces on CRE CLO market tone)

Additional Source Article = Quarter reporting and industry briefs cited in the article (Credaily / DBRS / Morningstar discussions of Q1/Q2 issuance). CRE Daily+1