Macroeconomic Factors Affecting Commercial Real Estate

August 5, 2025

Executive Summary

CRE in 2025 is being reshaped by high yet plateauing interest rates, inflation pressures, and shifting labor and capital markets. Amid these headwinds, self-storage stands out as a resilient segment—surging investment activity and stabilized cap rates bolster its defensive appeal.

Key points:

- Elevated interest rates raise cap rates, debt costs, and refinancing risk, though potential Fed rate cuts could revive transaction volume.

- Inflation has eased but operating and construction costs remain high; labor markets are tight but cooling, affecting sector-specific demand.

- Forecasted GDP growth (~1.4% - 1.9%) amid tightening credit squeezes deal liquidity and investor confidence.

- Tariffs, policy uncertainty, climate risk, and ESG pressures are adding complexity to valuations, insurance, and asset viability.

- Technology and AI reshape space needs; self-storage conversions offer adaptability and strong risk-adjusted returns.

Factors Impacting 2025 (and beyond)

Several macroeconomic factors are shaping the commercial real estate (CRE) market in 2025 and will likely continue influencing it in the years ahead. These broad, economy-wide forces impact investment, development, occupancy, financing, and valuation across property types (office, industrial, retail, multifamily, self-storage, etc.).

The following are some of the most significant factors effecting CRE now and in the future.

1. Interest Rates & Monetary Policy

High but stabilizing interest rates: The Federal Reserve has signaled a pause in rate hikes in 2025, but rates remain elevated compared to the past decade. This affects:

- Cap rates: Higher rates often lead to higher cap rates. Higher cap rates put greater pressure on what investors expect to earn from a CRE investment. A common method to achieve this is to decrease the asset value.

- Debt costs: Increased borrowing costs reduce deal activity and development feasibility.

- Refinancing risk: Properties acquired or financed during ultra-low rate periods may face distress if they borrowed more than the building revenue can support.

- The Federal Reserve operates under a dual mandate, which refers to the two key economic goals set by Congress: maximum employment and stable prices. Essentially, the Fed aims to foster an economy where as many people who want to work can find jobs, while also maintaining a low and stable rate of inflation.

- A "good" unemployment rate is generally considered to be between 4% and 6%, according to Investopedia and Forbes. This range is often referred to as "full employment" because it allows for a healthy level of job turnover and doesn't put excessive pressure on wages, according to the CEPR and Investopedia.

- The Federal Reserve (Fed) aims for a long-run inflation target of 2 percent, as measured by the annual change in the Personal Consumption Expenditures (PCE) price index. This target is a key component of their monetary policy strategy, which also includes a focus on maximum employment. The Fed's approach is often referred to as "flexible average inflation targeting".

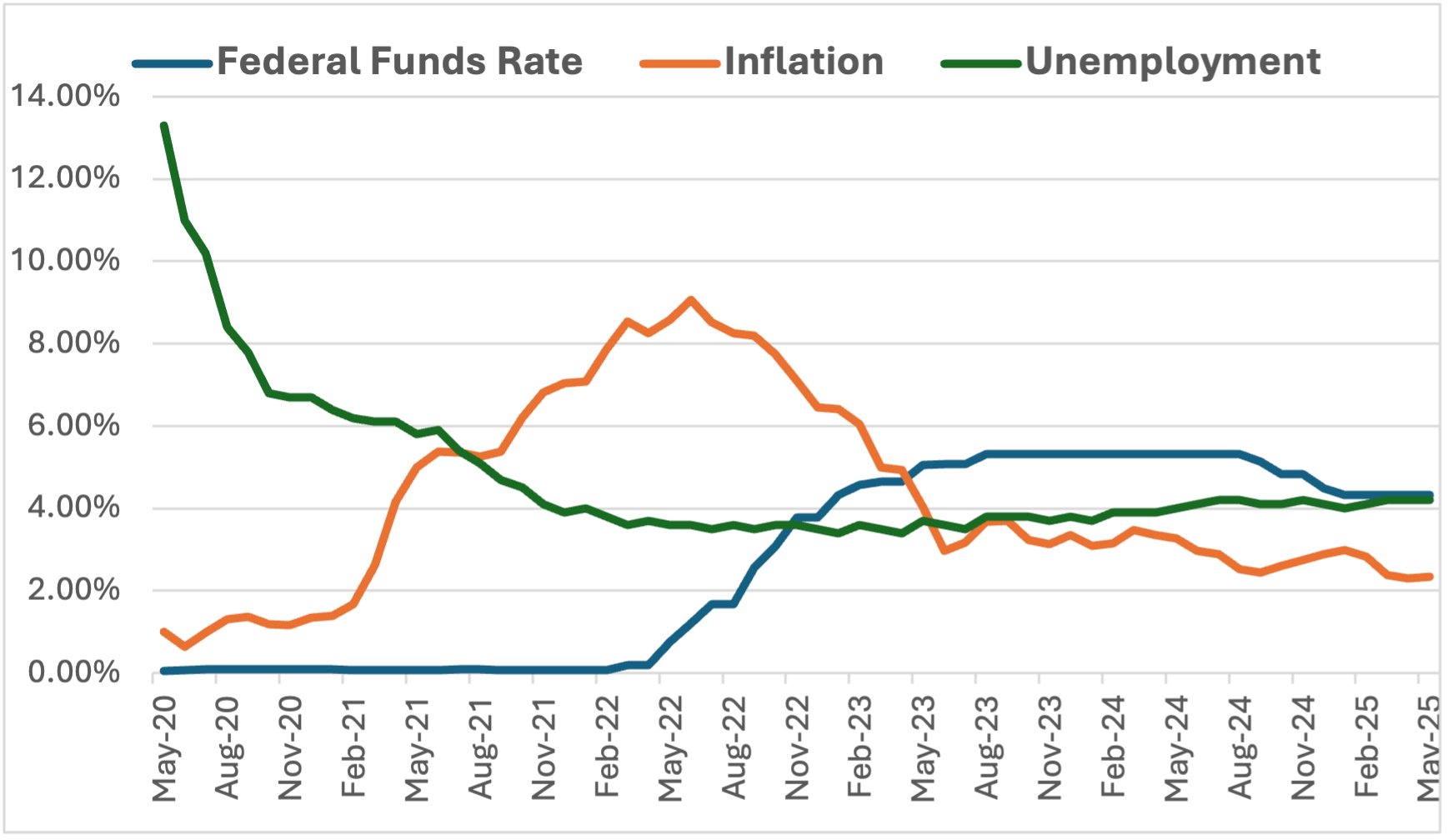

Below is a chart reflecting the relationship between inflation, unemployment, and the Fed funds rate over the past 5 years.

Given the highly unusual economic times during and after the pandemic, the interplay between these three economic factors is readily apparent. Understandably, The Federal Reserve waited to raise interest rates after the pandemic for several key reasons, primarily supporting the economic recovery and avoiding premature tightening. Additionally, their belief was that inflation was transitory, due to supply chain disruptions and shifts in consumer spending as the economy reopened.

However, the persistent and elevated inflation ultimately led the Fed to begin raising interest rates in March 2022, marking a shift in its policy approach. The impact of this move was seen almost immediately, and inflation rates began to drop from a high of over 9% in 2022, to around 2.4% currently.

Presently, the Federal Reserve has paused the easing of interest rates due to concern about inflation reaccelerating with potential weakening of the labor market, as well as economic uncertainties like those posed by tariffs and the lingering effects of past inflation. As the uncertainties about tax and tariff policies clear up, we will hopefully see a continued decline in interest rates later in the year.

Reductions in interest rates will stimulate CRE market activities in general and provide avenues to refinance more marginal holdings through improved valuations and lower finance costs. However, certain sectors like traditional Class B/C office, enclosed malls (unless repurposed) and urban multi-family will continue to face issues like high vacancy, remote work pressure, structural decline, affordability issues, and oversupply and continue to warrant caution and selectivity.

As of June 28, 2025, CME Fedwatch Tool put an 80.8% probability that the Fed will maintain interest rates in the upcoming meeting (July 30, 2025).

2. Inflation Trends

While inflation has cooled, it's still above pre-pandemic norms in some sectors.

- Rent escalations and operating costs (labor, utilities, insurance) are more volatile.

- Construction costs remain elevated due to global supply chain constraints and wage pressures. (This could be exacerbated by blanket tariffs currently proposed).

3. Labor Market Conditions

Tight but cooling labor markets continue to affect:

- Office demand: The rise of hybrid work models is reshaping office space requirements, potentially leading to lower demand for traditional office spaces while potentially boosting demand for other property types like industrial and logistics.

- Industrial demand: E-commerce logistics still require warehousing and distribution, though growth has normalized.

- Retail and hospitality: Labor shortages are improving but still constrain operations.

4. GDP Growth & Business Confidence

A healthy and growing economy, characterized by increased corporate investment and consumer spending, generally supports demand for commercial real estate across various sectors.

- Corporate profits affect tenant expansion decisions.

- Consumer spending drives retail and hospitality performance.

- A soft landing scenario boosts long-term investor confidence.

GDP forecasts for 2025 generally range from 1.4% (Philadelphia Fed) to 1.9% (IMF), with most predictions for 2026 continuing a sub-2% trend.

In summary, most forecasts point to moderate expansion with downside risks from tariffs, inflation pressures, and recession concerns.

Given this environment, CRE investment in high growth and/or recession resistant regions or industries will help provide risk mitigation while still targeting solid returns.

5. Capital Market Liquidity

CRE capital markets are cautious:

- Banks have tightened lending standards, especially regional and smaller lenders.

- Private equity and institutional investors are selective, seeking distressed opportunities and high-quality core assets.

- Foreign investment is mixed—selective inflows from Asia and the Middle East persist, but outbound capital is down.

6. Demographic Trends

Aging populations and millennial family formation influence:

- Multifamily demand: Remains strong in Sun Belt and secondary markets.

- Healthcare real estate: Growing need for medical office, senior housing, and life sciences.

- Retail mix: Shifting toward service-oriented tenants (gyms, clinics, entertainment).

7. Geopolitical Risks and Supply Chains

Ongoing global tensions (China–Taiwan, Russia–Ukraine, Red Sea disruptions) and nearshoring trends affect:

- Industrial real estate: Continued reshoring and domestic warehousing demand.

- Construction timelines and costs: Exposure to global materials and labor markets.

8. Government Policies

Changes in government policies related to trade, taxation, and environmental regulations can have significant consequences for the commercial real estate sector. All of these factors are seeing significant change in 2025, but the landscape is beginning to show signs of clearing:

- Passage of the Big Beautiful Bill on July 3, extends or makes permanent many real estate favorable provisions of the 2017 Tax Cuts & Jobs Act, including reinstatement of bonus depreciation and extension of the Qualified Opportunity Zone Program. The bill also includes expansion of the Low-Income Housing Tax Credit (LIHTC) and other provisions aimed at incentivizing affordable housing.

- On the trade front, Tariffs loom large

9. Climate Risk and ESG Regulation

Increasing climate-related regulations and investor pressure are pushing:

- Green building retrofits and sustainability-linked financing.

- Valuation discounts for non-compliant or high-risk assets.

- Rising insurance costs and risk mitigation expenses, particularly in coastal and wildfire-prone regions.

10. Technology & AI Adoption

Rapid AI and automation adoption is altering space demand:

- Office: Tech firms driving flexible space use and smaller footprints.

- Industrial: AI logistics improving warehouse efficiency.

- Retail: More omnichannel integration and data-driven layouts.

Overall Outlook:

The commercial real estate market in 2025 is expected to be dynamic and influenced by a complex interplay of macroeconomic factors and sector-specific trends. While some sectors may face challenges, others are poised for growth. Investors and developers who can adapt to changing market conditions, embrace technology, and focus on quality and location will be well-positioned for success.

Despite these headwinds, the self-storage sector demonstrates remarkable resilience, with investment sales reaching $855 million in Q1 2025—a 37% increase year-over-year—while cap rates have stabilized in the mid-5% to low-6% range.

Conclusion

The macroeconomic factors shaping commercial real estate in 2025 create a compelling case for strategic allocation to the self-storage sector, particularly through conversion investment strategies. While traditional commercial real estate faces headwinds from elevated interest rates, debt maturity pressures, and structural demand shifts, self-storage demonstrates fundamental resilience supported by demographic trends, supply discipline, and operational flexibility.

As traditional commercial real estate grapples with refinancing challenges and occupancy pressures, self-storage conversions offer a pathway to attractive risk-adjusted returns while providing essential infrastructure for evolving consumer storage needs.